EX-99.1

Published on November 18, 2014

| Exhibit 99.1

|

Lender Presentation November 18, 2014

|

|

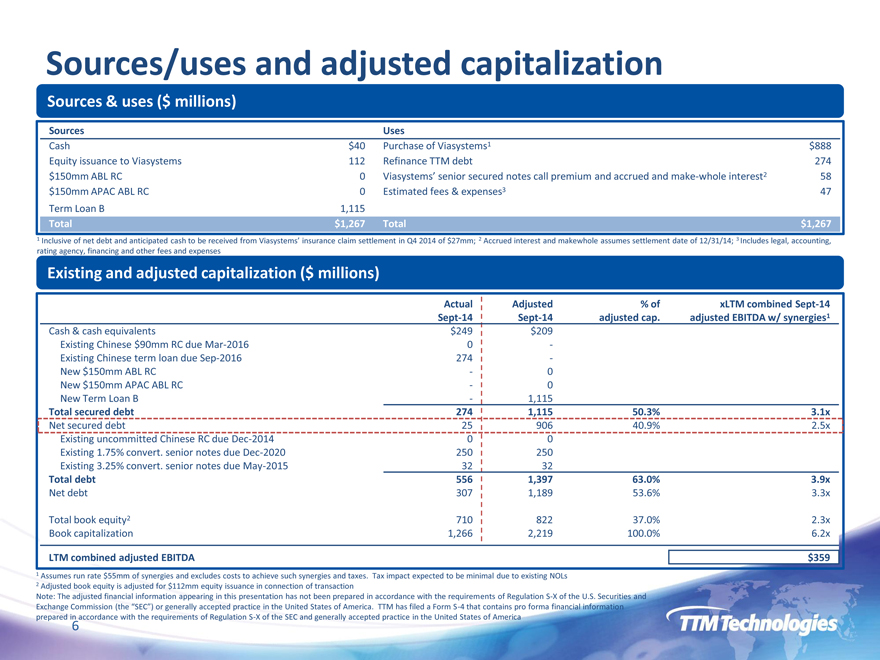

Sources/uses and adjusted capitalization

Sources & uses ($ millions)

Sources Uses

Cash $40 Purchase of Viasystems1 $888

Equity issuance to Viasystems 112 Refinance TTM debt 274

$150mm ABL RC 0 Viasystems senior secured notes call premium and accrued and make-whole interest2 58

$150mm APAC ABL RC 0 Estimated fees & expenses3 47

Term Loan B 1,115

Total $1,267 Total $1,267

1 Inclusive of net debt and anticipated cash to be received from Viasystems insurance claim settlement in Q4 2014 of $27mm; 2 Accrued interest and makewhole assumes settlement date of 12/31/14; 3 Includes legal, accounting, rating agency, financing and other fees and expenses

Existing and adjusted capitalization ($ millions)

Actual Adjusted% of xLTM combined Sept-14

Sept-14 Sept-14 adjusted cap. adjusted EBITDA w/ synergies1

Cash & cash equivalents $249 $209

Existing Chinese $90mm RC due Mar-2016 0 -

Existing Chinese term loan due Sep-2016 274 -

New $150mm ABL RC0

New $150mm APAC ABL RC0

New Term Loan B1,115

Total secured debt 274 1,115 50.3% 3.1x

Net secured debt 25 906 40.9% 2.5x

Existing uncommitted Chinese RC due Dec-2014 0 0

Existing 1.75% convert. senior notes due Dec-2020 250 250

Existing 3.25% convert. senior notes due May-2015 32 32

Total debt 556 1,397 63.0% 3.9x

Net debt 307 1,189 53.6% 3.3x

Total book equity2 710 822 37.0% 2.3x

Book capitalization 1,266 2,219 100.0% 6.2x

LTM combined adjusted EBITDA $359

1 Assumes run rate $55mm of synergies and excludes costs to achieve such synergies and taxes. Tax impact expected to be minimal due to existing NOLs

2 Adjusted book equity is adjusted for $112mm equity issuance in connection of transaction

Note: The adjusted financial information appearing in this presentation has not been prepared in accordance with the requirements of Regulation S-X of the U.S. Securities and

Exchange Commission (the SEC) or generally accepted practice in the United States of America. TTM has filed a Form S-4 that contains pro forma financial information prepared in accordance with the requirements of Regulation S-X of the SEC and generally accepted practice in the United States of America

6

|

|

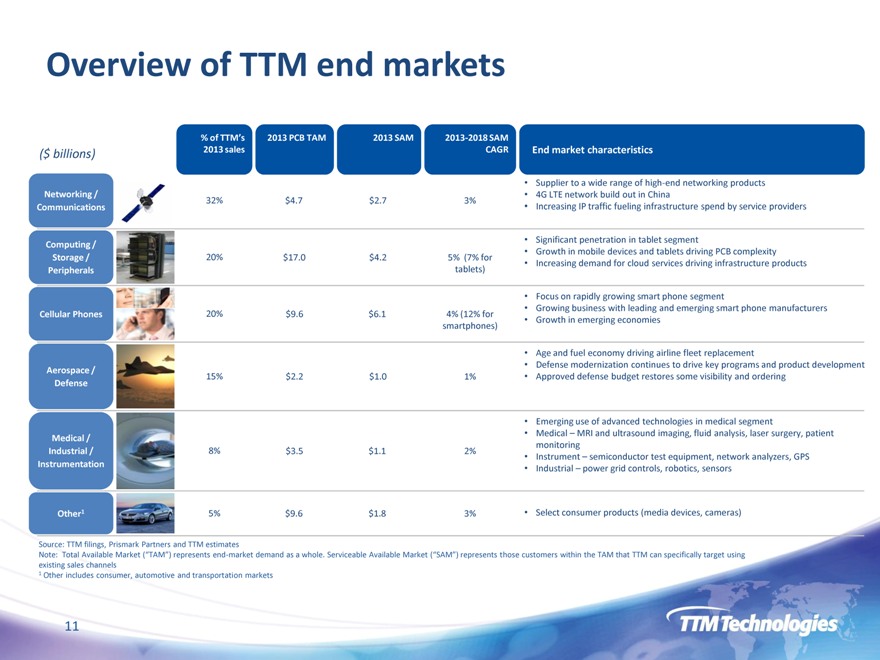

Overview of TTM end markets

% of TTMs 2013 PCB TAM 2013 SAM 2013-2018 SAM

($ billions) 2013 sales CAGR End market characteristics

Supplier to a wide range of high-end networking products

Networking / 4G LTE network build out in China

32% $4.7 $2.7 3%

Communications Increasing IP traffic fueling infrastructure spend by service providers

Computing / Significant penetration in tablet segment

Growth in mobile devices and tablets driving PCB complexity

Storage / 20% $17.0 $4.2 5% (7% for Increasing demand for cloud services driving infrastructure products

Peripherals tablets)

Focus on rapidly growing smart phone segment

Growing business with leading and emerging smart phone manufacturers

Cellular Phones 20% $9.6 $6.1 4% (12% for Growth in emerging economies

smartphones)

Age and fuel economy driving airline fleet replacement

Defense modernization continues to drive key programs and product development

Aerospace / 15% $2.2 $1.0 1% Approved defense budget restores some visibility and ordering

Defense

Emerging use of advanced technologies in medical segment

Medical / Medical MRI and ultrasound imaging, fluid analysis, laser surgery, patient

monitoring

Industrial / 8% $3.5 $1.1 2% Instrument semiconductor test equipment, network analyzers, GPS

Instrumentation Industrial power grid controls, robotics, sensors

Other1 5% $9.6 $1.8 3% Select consumer products (media devices, cameras)

Source: TTM filings, Prismark Partners and TTM estimates

Note: Total Available Market (TAM) represents end-market demand as a whole. Serviceable Available Market (SAM) represents those customers within the TAM that TTM can specifically target using

existing sales channels

1 Other includes consumer, automotive and transportation markets

11

|

|

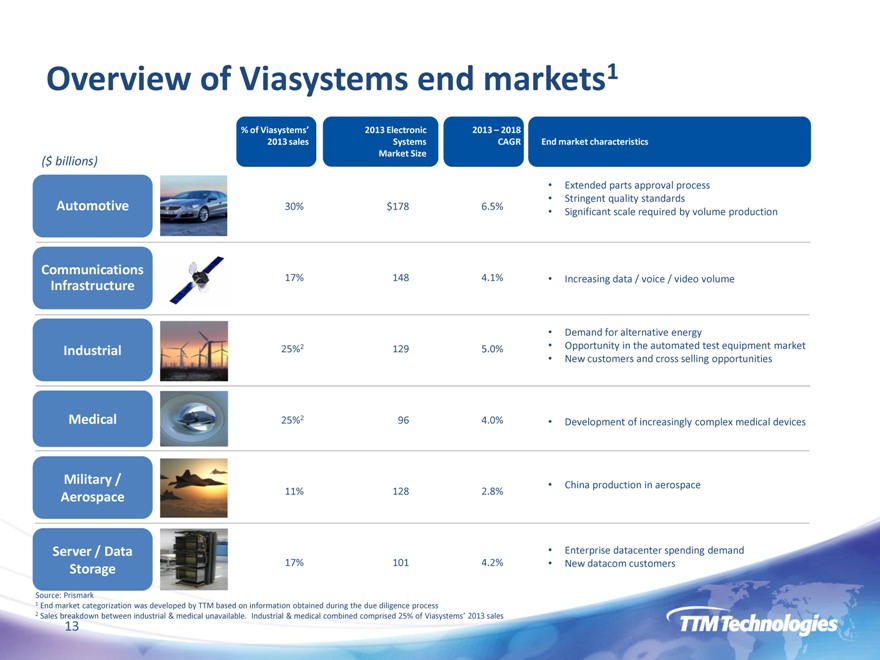

Overview of Viasystems end markets1

% of Viasystems 2013 Electronic 2013 2018

2013 sales Systems CAGR End market characteristics

Market Size

($ billions)

Extended parts approval process

Stringent quality standards

Automotive 30% $178 6.5% Significant scale required by volume production

Communications

Infrastructure 17% 148 4.1% Increasing data / voice / video volume

Demand for alternative energy

Industrial 25%2 129 5.0% Opportunity in the automated test equipment market

New customers and cross selling opportunities

Medical 25%2 96 4.0% Development of increasingly complex medical devices

Military / China production in aerospace

Aerospace 11% 128 2.8%

Server / Data Enterprise datacenter spending demand

Storage 17% 101 4.2% New datacom customers

Source: Prismark

1 End market categorization was developed by TTM based on information obtained during the due diligence process

2 Sales breakdown between industrial & medical unavailable. Industrial & medical combined comprised 25% of Viasystems 2013 sales

13

|

|

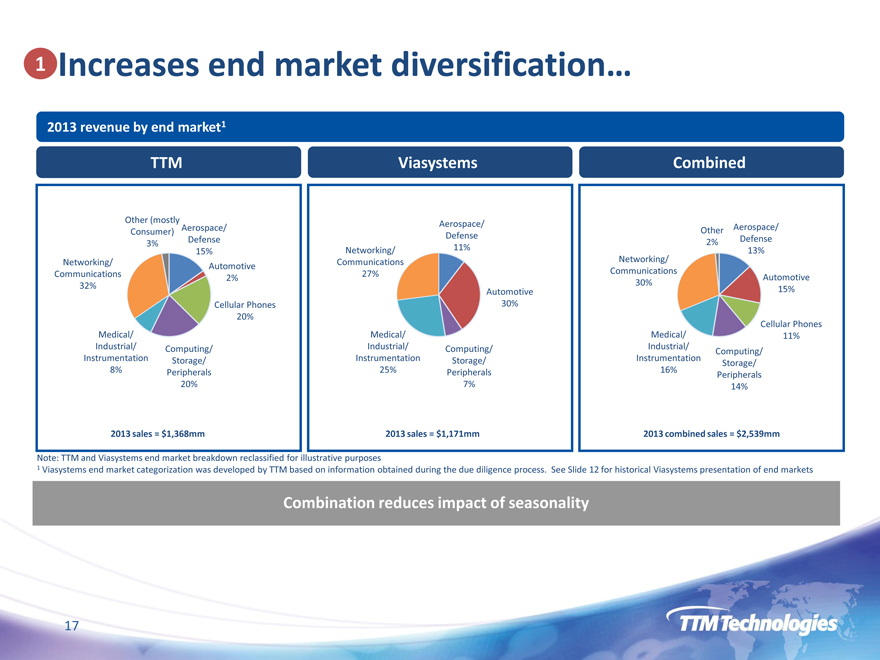

1 Increases end market diversification

2013 revenue by end market1

TTM Viasystems Combined

Other (mostly

Consumer) Aerospace/

3% Defense

15%

Networking/ Automotive

Communications 2%

32%

Cellular Phones

20%

Medical/

Industrial/ Computing/

Instrumentation Storage/

8% Peripherals

20%

2013 sales = $1,368mm

Aerospace/

Defense

Networking/ 11%

Communications

27%

Automotive

30%

Medical/

Industrial/ Computing/

Instrumentation Storage/

25% Peripherals

7%

2013 sales = $1,171mm

Other Aerospace/

2% Defense

13%

Networking/

Communications

30% Automotive

15%

Cellular Phones

Medical/ 11%

Industrial/ Computing/

Instrumentation Storage/

16% Peripherals

14%

2013 combined sales = $2,539mm

Note: TTM and Viasystems end market breakdown reclassified for illustrative purposes

1 Viasystems end market categorization was developed by TTM based on information obtained during the due diligence process. See Slide 12 for historical Viasystems presentation of end markets

Combination reduces impact of seasonality

17

|

|

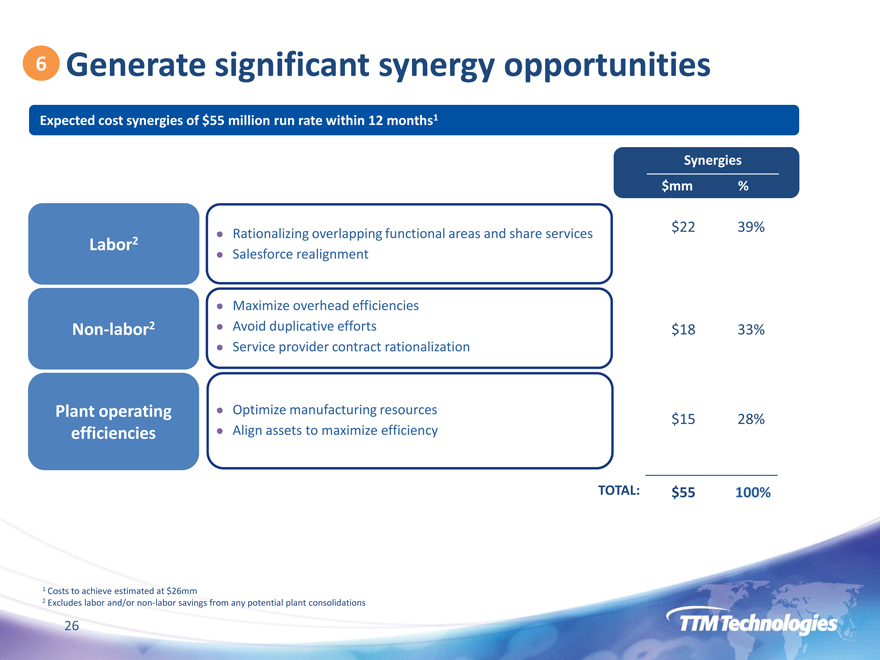

6 Generate significant synergy opportunities

Expected cost synergies of $55 million run rate within 12 months1

Labor2

Non-labor2

Plant operating

efficiencies

Rationalizing overlapping functional areas and share services

Salesforce realignment

Maximize overhead efficiencies

Avoid duplicative efforts

Service provider contract rationalization

Optimize manufacturing resources

Align assets to maximize efficiency

Synergies

$mm%

$22 39%

$18 33%

$15 28%

TOTAL: $55 100%

1 Costs to achieve estimated at $26mm

2 Excludes labor and/or non-labor savings from any potential plant consolidations

26

|

|

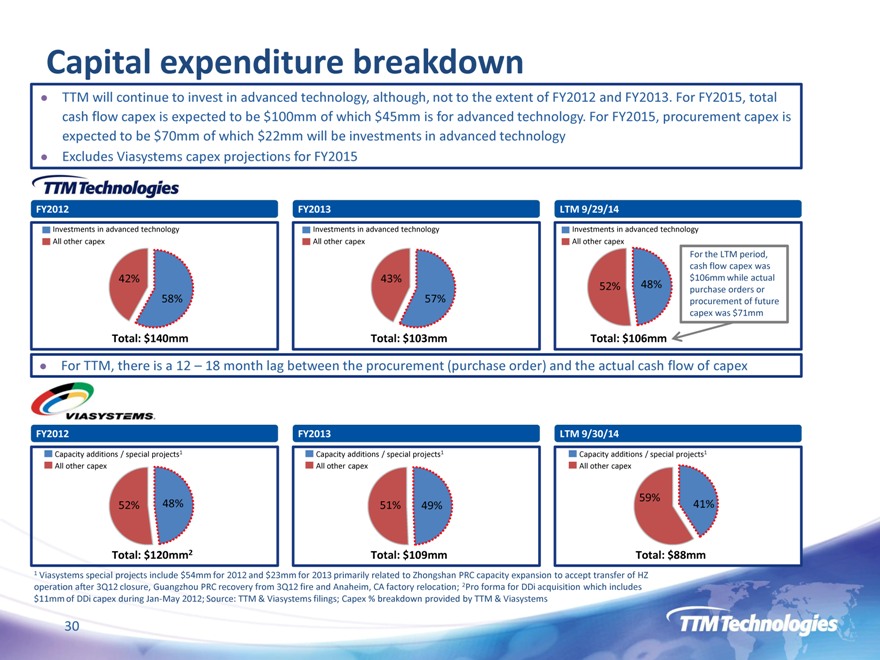

Capital expenditure breakdown

TTM will continue to invest in advanced technology, although, not to the extent of FY2012 and FY2013. For FY2015, total

cash flow capex is expected to be $100mm of which $45mm is for advanced technology. For FY2015, procurement capex is

expected to be $70mm of which $22mm will be investments in advanced technology

Excludes Viasystems capex projections for FY2015

FY2012 FY2013 LTM 9/29/14

Investments in advanced technology Investments in advanced technology Investments in advanced technology

All other capex All other capex All other capex

For the LTM period,

cash flow capex was

42% 43% $106mm while actual

52% 48% purchase orders or

58% 57% procurement of future

capex was $71mm

Total: $140mm Total: $103mm Total: $106mm

For TTM, there is a 12 18 month lag between the procurement (purchase order) and the actual cash flow of capex

FY2012 FY2013 LTM 9/30/14

Capacity additions / special projects1 Capacity additions / special projects1 Capacity additions / special projects1

All other capex All other capex All other capex

59%

52% 48% 51% 49% 41%

Total: $120mm2 Total: $109mm Total: $88mm

1 Viasystems special projects include $54mm for 2012 and $23mm for 2013 primarily related to Zhongshan PRC capacity expansion to accept transfer of HZ

operation after 3Q12 closure, Guangzhou PRC recovery from 3Q12 fire and Anaheim, CA factory relocation; 2Pro forma for DDi acquisition which includes

30