EX-99.1

Published on May 8, 2003

Exhibit 99.1

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Searchable text section of graphics shown above

JP Morgan Technology & Telecom Conference

May 8, 2003

[LOGO]

During the course of this presentation, we will make projections or other forward-looking statements regarding future events or the future financial performance of the Company. We wish to caution you that such statements reflect only our current expectations, and that actual events or results may differ materially.

We refer you to the risk factors and cautionary language contained in the documents that the Company files from time to time with the Securities and Exchange Commission, specifically the Companys 10-K for our last fiscal year ended December 31, 2002. Such documents contain and identify important factors that could cause the actual results to differ materially from those contained in our projections or forward-looking statements. We undertake no obligation to update such projections or such forward-looking statements in the future.

For your convenient reference, a copy of this presentation on Form 8-K has been filed with the Securities and Exchange Commission and will be posted on our website.

President

and

Chief Executive Officer

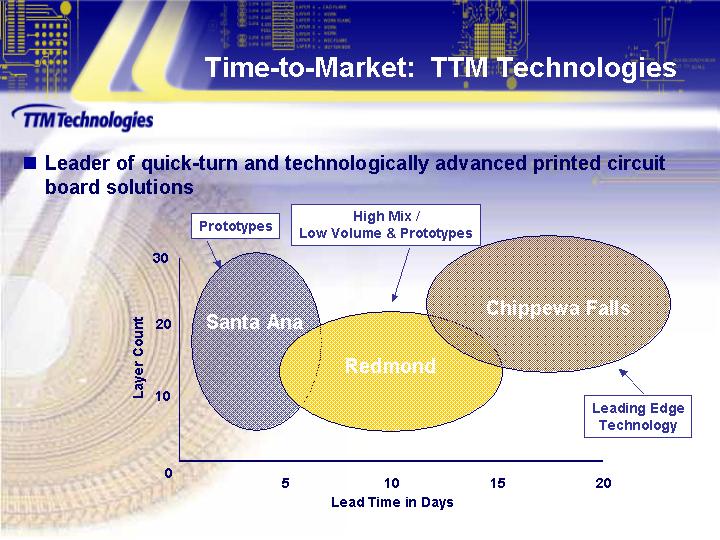

Time-to-Market: TTM Technologies

Leader of quick-turn and technologically advanced printed circuit board solutions

[CHART]

Advantages

of

Time and

Technology

Faster Growth

Access to more diversified customer base

Critical to NPI across industries

Superior margins and profitability

Significant barriers to entry

Unique capabilities and culture for time

Significant investment and expertise for technology

Few competitors in either target market segment

Industry leading financial performance

Most profitable business model through the cycle

Strong balance sheet

Lowest domestic cost structure

Focus on most attractive PCB industry niches

Time and technology

Recent ACI acquisition surpasses high-technology positioning in the market

Well positioned for industry upturn

Diversified customers and end-markets

Ability to double revenues without additional capital investment

Proven ability to integrate acquisitions

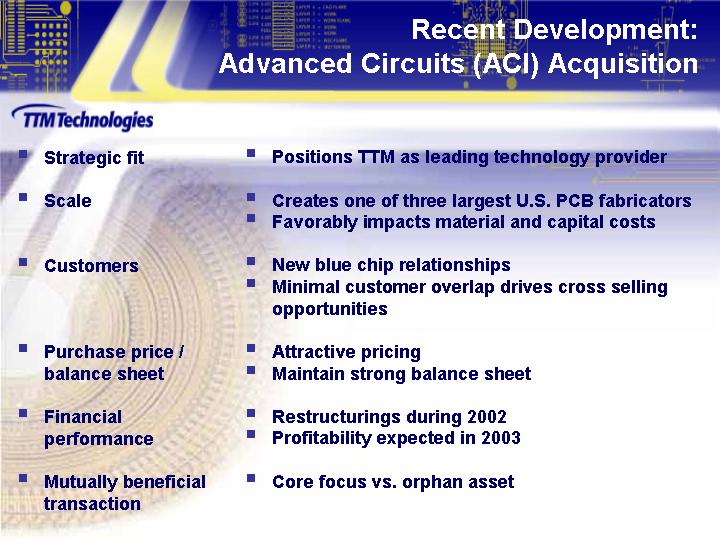

Advanced Circuits (ACI) Acquisition

|

Strategic fit |

|

Positions TTM as leading technology provider |

|

|

|

|

|

Scale |

|

Creates one of three largest U.S. PCB

fabricators |

|

|

|

|

|

Customers |

|

New blue chip relationships |

|

|

|

|

|

Purchase price / balance sheet |

|

Attractive pricing |

|

|

|

|

|

Financial performance |

|

Restructurings during 2002 |

|

|

|

|

|

Mutually beneficial transaction |

|

Core focus vs. orphan asset |

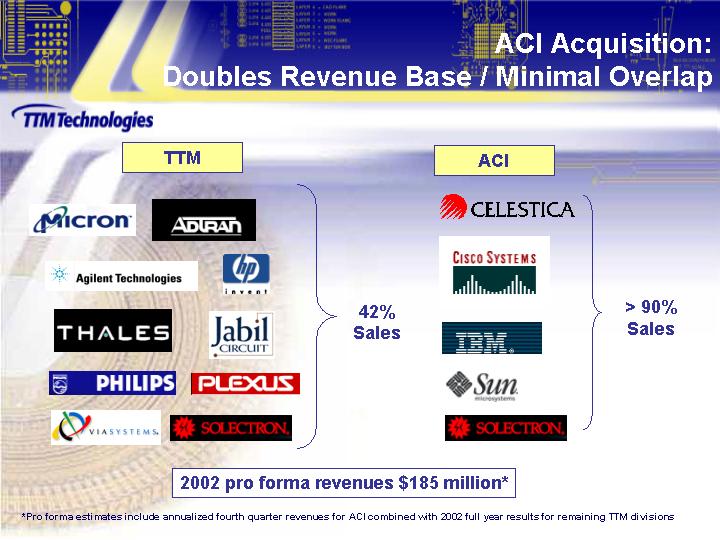

Doubles Revenue Base / Minimal Overlap

|

TTM |

|

|

|

ACI |

|

|

|

|

[LOGOS] |

|

42% |

|

[LOGOS] |

|

> 90% |

|

|

2002 pro forma revenues $185 million* |

* Pro forma estimates include annualized fourth quarter revenues for ACI combined with 2002 full year results for remaining TTM divisions

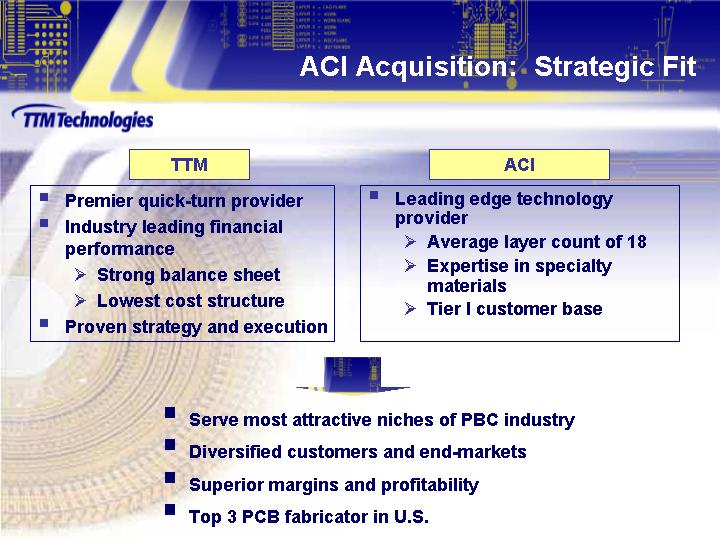

ACI Acquisition: Strategic Fit

|

TTM |

|

ACI |

|

|

Premier quick-turn provider |

|

Leading edge technology provider |

|

|

Industry leading financial performance |

|

Average layer count of 18 |

|

|

Strong balance sheet |

|

Expertise in specialty materials |

|

|

Lowest cost structure |

|

Tier I customer base |

|

|

Proven strategy and execution |

|

|

|

[GRAPHIC]

|

|

|

Serve most attractive niches of PBC industry |

|

|

|

Diversified customers and end-markets |

|

|

|

Superior margins and profitability |

|

|

|

Top 3 PCB fabricator in U.S. |

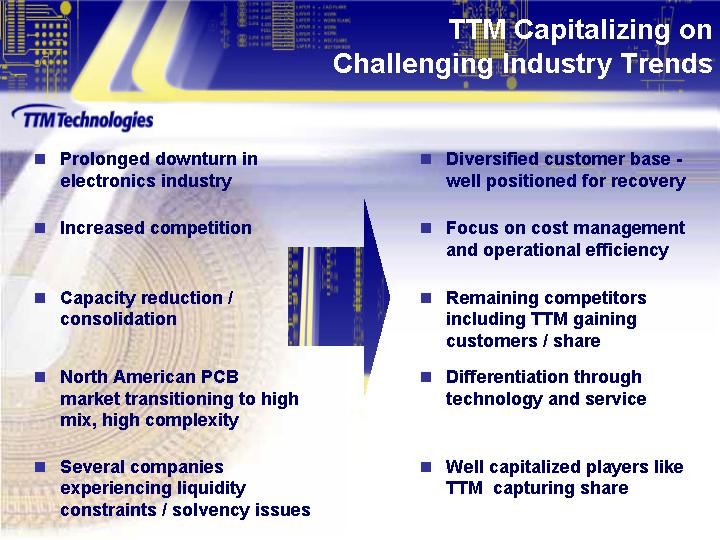

TTM

Capitalizing on

Challenging

Industry Trends

|

Prolonged downturn in electronics industry |

|

Diversified customer basewell positioned for recovery |

|

|

|

|

|

Increased competition |

|

Focus on cost management and operational efficiency |

|

|

|

|

|

Capacity reduction / consolidation [GRAPHIC] |

|

Remaining competitors including TTM gaining customers / share |

|

|

|

|

|

North American PCB market transitioning to high mix, high complexity |

|

Differentiation through technology and service |

|

|

|

|

|

Several companies experiencing liquidity constraints / solvency issues |

|

Well capitalized players like TTM capturing share |

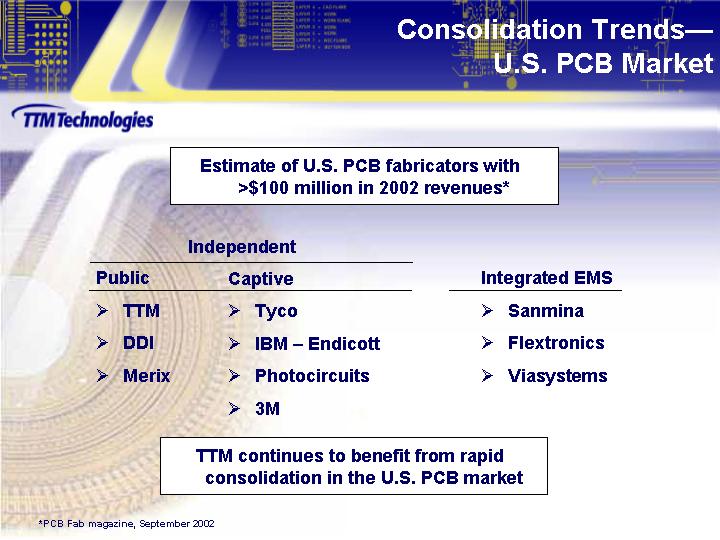

Consolidation

Trends

U.S. PCB Market

|

Estimate of U.S. PCB fabricators with |

|

Independent |

|

|

|

||

|

Public |

|

Captive |

|

Integrated EMS |

|

|

TTM |

|

Tyco |

|

Sanmina |

|

|

|

|

|

|

|

|

|

DDI |

|

IBM Endicott |

|

Flextronics |

|

|

|

|

|

|

|

|

|

Merix |

|

Photocircuits |

|

Viasystems |

|

|

|

|

|

|

|

|

|

|

|

3M |

|

|

|

|

TTM continues to benefit from rapid |

* PCB Fab magazine, September 2002

Capacity

Reductions:

30% - 35% Since

2001

|

Announced Plant Closings(1) |

|

Estimated Capacity Shutdown(2) |

|

|

2001 Total |

|

$1,655 |

|

|

|

|

|

|

|

2002 |

|

|

|

|

Sanmina (NH) |

|

$70 $80 |

|

|

Teradyne (CA) |

|

$60 $70 |

|

|

Omni Circuits (CA) |

|

$30 $35 |

|

|

Honeywell (Various U.S. Sites) |

|

$60 $100 |

|

|

Tyco Advanced Quick (FL) |

|

$60 |

|

|

Paragon Circuits (CA) |

|

$20 |

|

|

Carolina Circuits (SC) |

|

$40 |

|

|

Viasystems (Toronto) |

|

$50 |

|

|

Printed Circuit Corp (MA) |

|

$40 |

|

|

Flextronics / Multek (CA) |

|

$40 |

|

|

TTM Burlington (WA) |

|

$30 |

|

|

|

|

|

|

|

Total |

|

$2,155 - $2,220 |

|

Source: Research analysts / company estimates.

(1) Some facilities could re-open if demand improves, but this would require significant lead time and rebuilding of front-end capabilities.

(2) Measured in 2001 revenue.

|

|

|

|

|

|

|

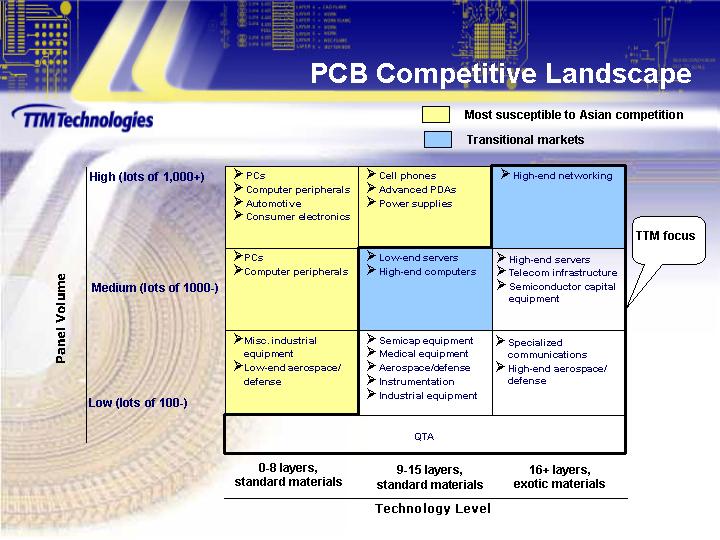

TTM focus |

||||||

|

Panel volume |

|

Most susceptible |

|

Most susceptible to Asian competition |

|

Transitional |

|

|

|

Transitional |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

High (lots of 1,000+) |

|

PCs |

|

Cell phones |

|

|

|

|

|

High-end networking |

|

|

|

|

|

Computer peripherals |

|

Advanced PDAs |

|

|

|

|

|

|

|

|

|

|

|

Automotive |

|

Power supplies |

|

|

|

|

|

|

|

|

|

|

|

Consumer electronics |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Medium (lots of 1000-) |

|

PCs |

|

|

|

Low-end servers |

|

|

|

High-end servers |

|

|

|

|

|

Computer peripherals |

|

|

|

High-end computers |

|

|

|

Telecom infrastructure |

|

|

|

|

|

|

|

|

|

|

|

|

|

Semiconductor capital equipment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Low (lots of 100-) |

|

Misc. industrial equipment |

|

|

|

Semicap equipment |

|

|

|

Specialized communications |

|

|

|

|

|

Low-end aerospace/defense |

|

|

|

Medical equipment |

|

|

|

High-end aerospace/ defense |

|

|

|

|

|

|

|

|

|

Aerospace/ defense |

|

|

|

|

|

|

|

|

|

|

|

|

|

Instrumentation |

|

|

|

|

|

|

|

|

|

|

|

|

|

Industrial equipment |

|

|

|

|

|

|

|

|

|

QTA |

||||||||||

|

|

|

0-8 layers, standard materials |

|

9-15 layers, standard materials |

|

16+ layers, exotic materials |

||||||

|

|

|

Technology Level |

||||||||||

TTMs Strategy

Industry-Leading

Financial Results

Strong Long-Term Outlook

Customers / End Markets

Diversified customer base of industry leading clients

Targeting emerging customers and end-markets

Expanded sales force

Time

24 hour turn-time capability

Prototype to mid-volume production in under 10 days

Ability to handle 40 45 new designs per day

Financial Strength

Strong balance sheet

Superior asset management

Opportunistic acquisitions

Technology

Specialization in high layer count, advanced technology PCBs

Provider of valued-added engineering / design services

ACIindustry leading layer count of 18

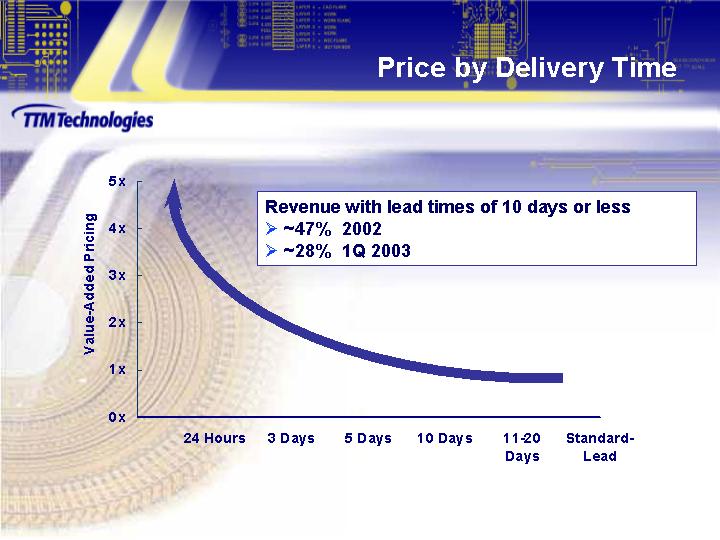

[CHART]

Revenue with lead times of 10 days or less

~47% 2002

~28% 1Q 2003

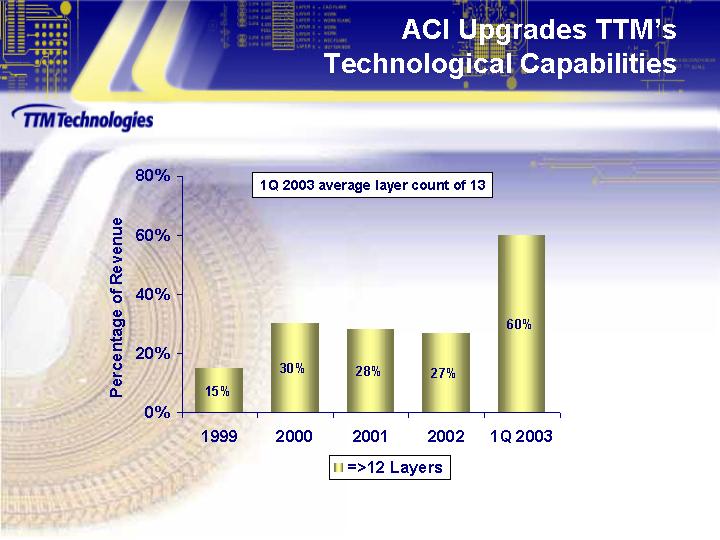

ACI

Upgrades TTMs

Technological

Capabilities

[CHART]

1Q 2003 average layer count of 13

Recognized

by

Industry Leaders

|

OEMs |

|

EMS Providers |

|

|

[LOGOS] |

|

[LOGOS] |

|

TTM

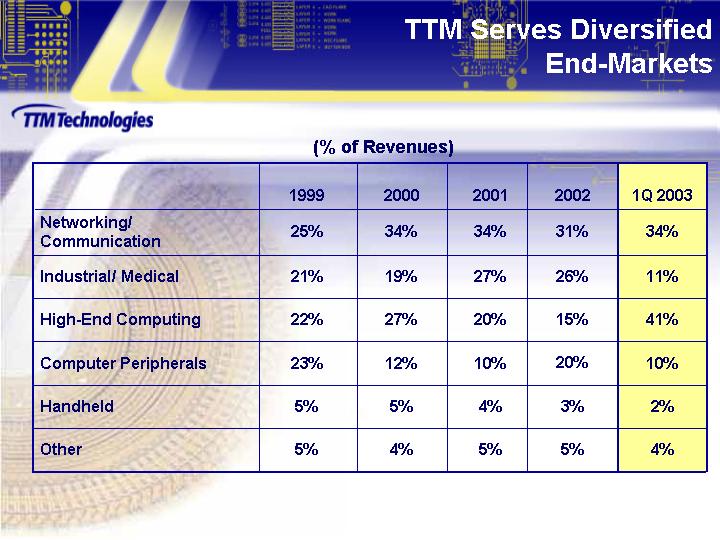

Serves Diversified

End-Markets

(% of Revenues)

|

|

|

1999 |

|

2000 |

|

2001 |

|

2002 |

|

1Q 2003 |

|

|

Networking/ Communication |

|

25% |

|

34% |

|

34% |

|

31% |

|

34% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Industrial/ Medical |

|

21% |

|

19% |

|

27% |

|

26% |

|

11% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

High-End Computing |

|

22% |

|

27% |

|

20% |

|

15% |

|

41% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Computer Peripherals |

|

23% |

|

12% |

|

10% |

|

20% |

|

10% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Handheld |

|

5% |

|

5% |

|

4% |

|

3% |

|

2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other |

|

5% |

|

4% |

|

5% |

|

5% |

|

4% |

|

Niche-oriented

Expand quick-turn market share

Expand specialty materials opportunities with military / aerospace end-market exposure

Develop profitable Asian relationship

Focus on PCB manufacturing

Chief Financial Officer

[CHART]

* Pro forma estimates include annualized fourth quarter revenues for ACI combined with 2002 full year results for remaining TTM divisions

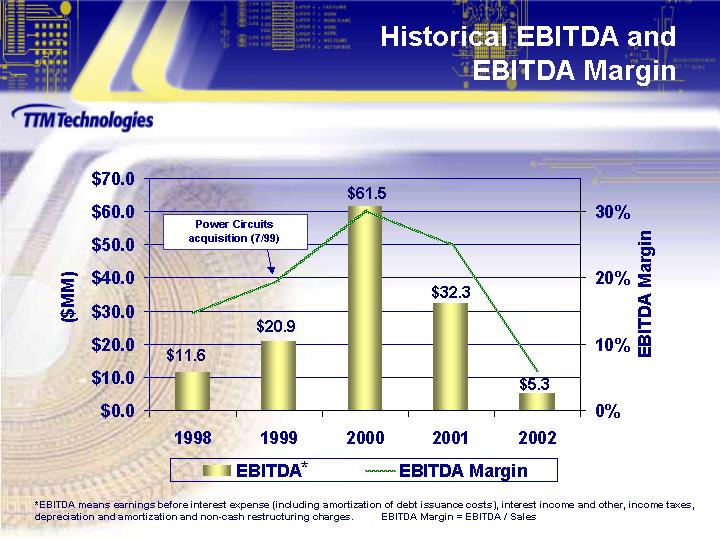

Historical

EBITDA and

EBITDA Margin

[CHART]

* EBITDA means earnings before interest expense (including amortization of debt issuance costs), interest income and other, income taxes, depreciation and amortization and non-cash restructuring charges. EBITDA Margin = EBITDA / Sales

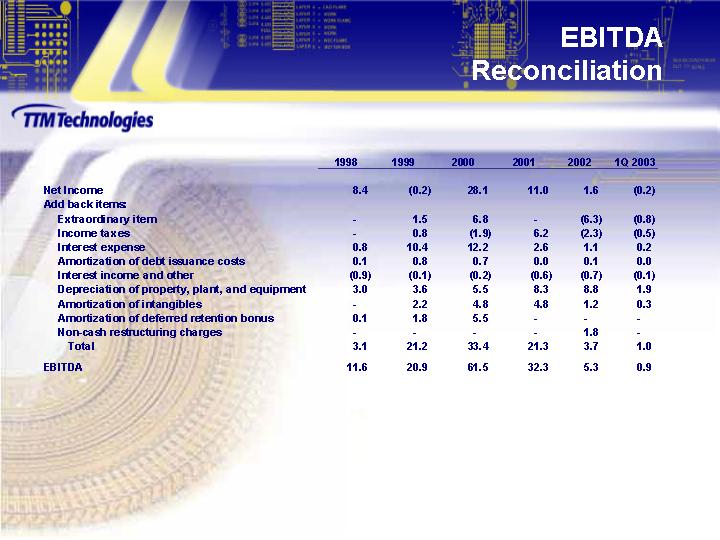

Reconciliation

|

|

|

1998 |

|

1999 |

|

2000 |

|

2001 |

|

2002 |

|

1Q 2003 |

|

|

Net Income |

|

8.4 |

|

(0.2) |

|

28.1 |

|

11.0 |

|

1.6 |

|

(0.2) |

|

|

Add back items: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Extraordinary item |

|

|

|

1.5 |

|

6.8 |

|

|

|

(6.3) |

|

(0.8) |

|

|

Income taxes |

|

|

|

0.8 |

|

(1.9) |

|

6.2 |

|

(2.3) |

|

(0.5) |

|

|

Interest expense |

|

0.8 |

|

10.4 |

|

12.2 |

|

2.6 |

|

1.1 |

|

0.2 |

|

|

Amortization of debt issuance costs |

|

0.1 |

|

0.8 |

|

0.7 |

|

0.0 |

|

0.1 |

|

0.0 |

|

|

Interest income and other |

|

(0.9) |

|

(0.1) |

|

(0.2) |

|

(0.6) |

|

(0.7) |

|

(0.1) |

|

|

Depreciation of property, plant, and equipment |

|

3.0 |

|

3.6 |

|

5.5 |

|

8.3 |

|

8.8 |

|

1.9 |

|

|

Amortization of intangibles |

|

|

|

2.2 |

|

4.8 |

|

4.8 |

|

1.2 |

|

0.3 |

|

|

Amortization of deferred retention bonus |

|

0.1 |

|

1.8 |

|

5.5 |

|

|

|

|

|

|

|

|

Non-cash restructuring charges |

|

|

|

|

|

|

|

|

|

1.8 |

|

|

|

|

Total |

|

3.1 |

|

21.2 |

|

33.4 |

|

21.3 |

|

3.7 |

|

1.0 |

|

|

EBITDA |

|

11.6 |

|

20.9 |

|

61.5 |

|

32.3 |

|

5.3 |

|

0.9 |

|

|

|

|

FIRST QUARTER |

|

||

|

Dollars in millions, except per share data |

|

2002 |

|

2003 |

|

|

Sales |

|

$ 23.7 |

|

$ 39.6 |

|

|

|

|

|

|

|

|

|

Gross Profit |

|

2.6 |

|

4.5 |

|

|

|

|

|

|

|

|

|

Operating Profit |

|

(0.2) |

|

(1.3) |

|

|

|

|

|

|

|

|

|

Net Income Before Extraordinary* |

|

(0.3) |

|

(0.8) |

|

|

|

|

|

|

|

|

|

EPS Before Extraordinary* |

|

$ (0.01) |

|

$ (0.02) |

|

|

|

|

|

|

|

|

|

Operating Cash Flow |

|

$ 3.9 |

|

$ 7.8 |

|

|

|

|

|

|

|

|

|

Inventory Turns |

|

26x |

|

14x |

|

* 1Q 2003 results includes $203,000 restructuring charge and are before extraordinary gain of $824,000, related to acquisition of ACI

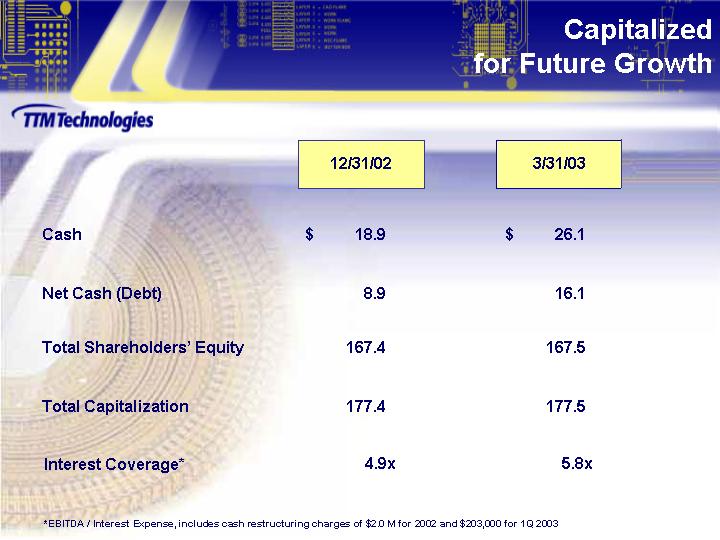

for Future Growth

|

|

|

12/31/02 |

|

3/31/03 |

|

|

Cash |

|

$ 18.9 |

|

$ 26.1 |

|

|

|

|

|

|

|

|

|

Net Cash (Debt) |

|

8.9 |

|

16.1 |

|

|

|

|

|

|

|

|

|

Total Shareholders Equity |

|

167.4 |

|

167.5 |

|

|

|

|

|

|

|

|

|

Total Capitalization |

|

177.4 |

|

177.5 |

|

|

|

|

|

|

|

|

|

Interest Coverage* |

|

4.9x |

|

5.8x |

|

* EBITDA / Interest Expense, includes cash restructuring charges of $2.0 M for 2002 and $203,000 for 1Q 2003

Proven, industry-leading execution

ACI acquisition establishes TTM as leading technology provider

Well-positioned for industry recovery as one of the largest U.S. PCB fabricators

Investing in time and technology

Positioned to gain market share as industry winner

Strong balance sheet